Engineering the Clock: Institutional Advantages of Long Term Tempo Control

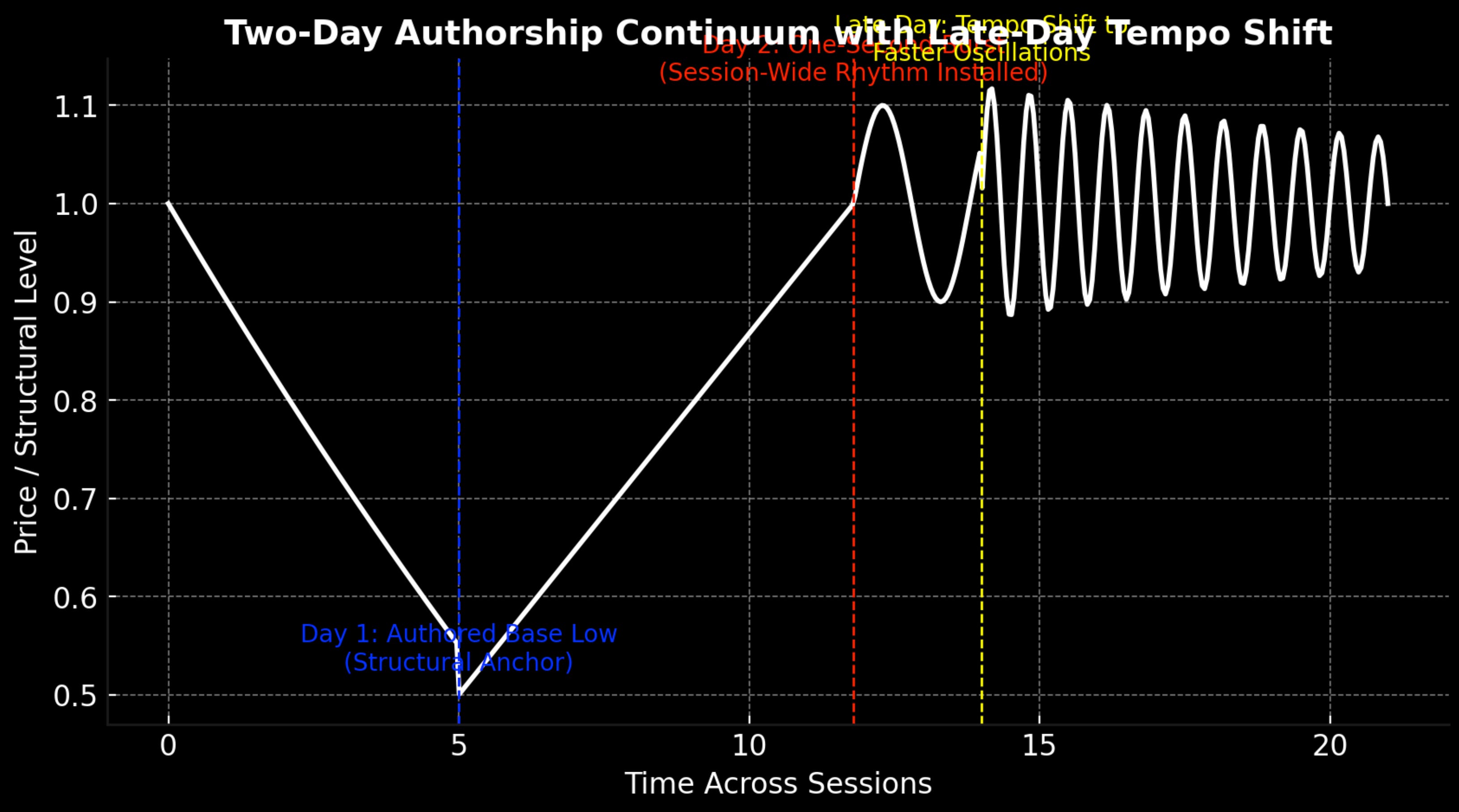

Today’s market wasn’t a sequence of trades.

It was a single authored continuum.

Across 24 hours, three distinct authored interventions defined — and redefined — the market’s tempo: